As the Occupy Wall Street movement gathers momentum and money, Wall Street itself is losing both. The swift collapse and bankruptcy of trading firm MF Global is testament to that, and—while like all unhappy families it has its own peculiar story—its failure is also emblematic of the spiral of declining profits that is rendering Wall Street a shadow of what it was just a few years ago.

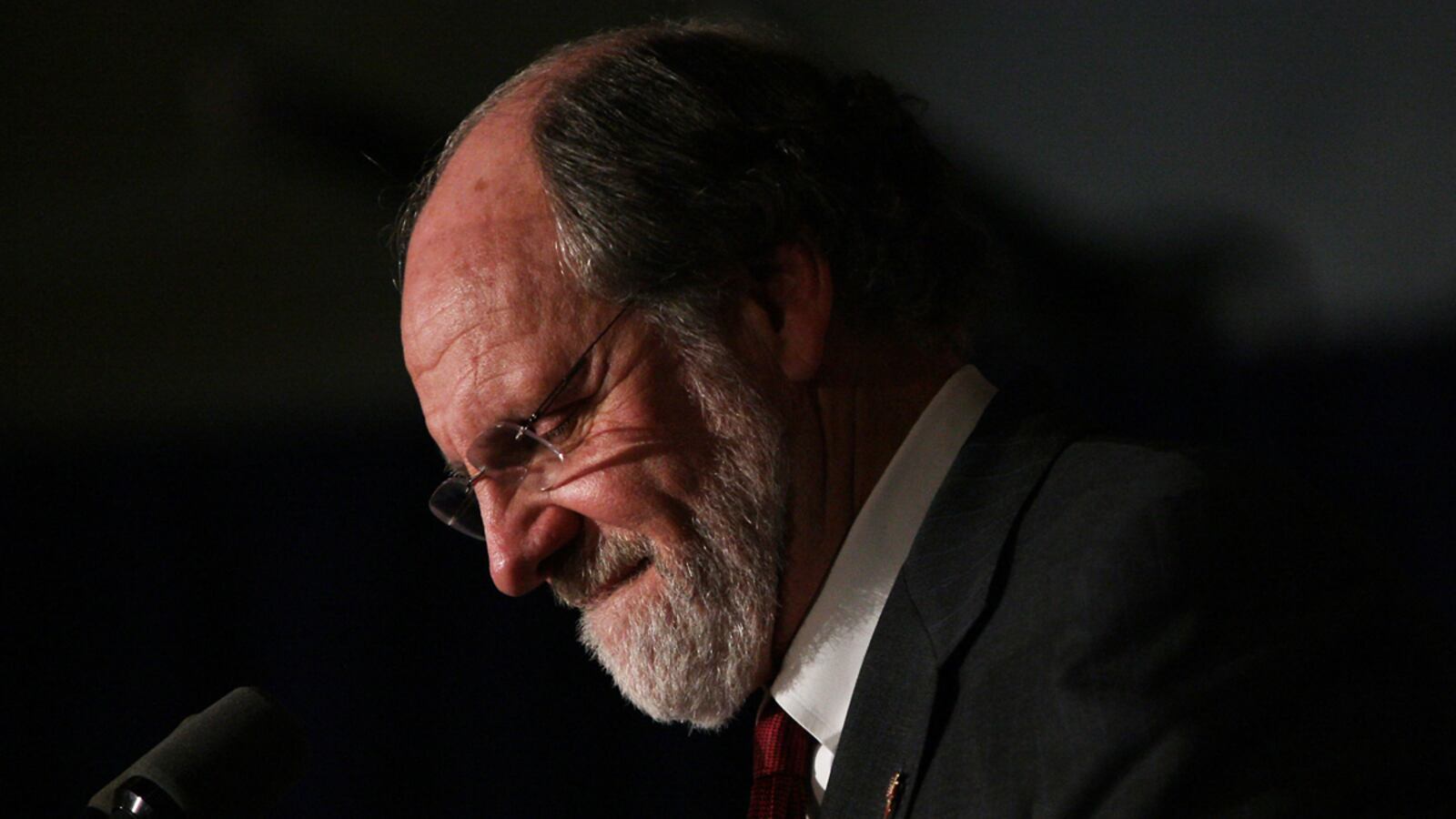

It is tempting to make the failure of MF Global into a passion play of its high-profile CEO, Jon Corzine, former senator and ex-governor of New Jersey, and former head of Goldman Sachs. As Charles Gasparino noted, Corzine is a decent man with a stellar résumé and undoubted success in the world of business and politics, yet he has presided over major failures at Goldman in the 1990s and now at MF. His political career is equally mixed: yes, he got elected twice by the good voters of New Jersey, but he was then vehemently booted by those same voters who preferred the histrionics and no-b.s. demeanor of Chris Christie.

Corzine undoubtedly and most unwisely encouraged risk at MF Global. As we know now, that entailed taking $6.3 billion in short-term positions on European sovereign debt just as the euro zone was plunged into yet another phase of its multiyear crisis by the near-default of Greece. That $6.3 billion was five times the entire tangible equity of MF Global, and was only possible through a leveraged bet that Corzine had to have countenanced. Betting five times your firm on risky bonds can make you a fortune. It can also go bad quickly, and for Corzine it did, bringing down the remnants of a firm whose origins stretch back to the beginning of the 19th century and the heyday of the British Empire.

As was true with the even greater leverage that brought down Lehman Brothers and chunks of the financial system in late 2008, the failure of MF Global is another numbing example of risk run amok. The major investment banks and trading firms have lessened their tendency to bet the proverbial farm because they recognize that only mayhem and loss can come of it, as the sorry story of Corzine and MF Global demonstrates.

Yes, the J.P. Morgans and Citis of the world have pared back risk and exposure, in part due to more stringent capital regulations for depository banks, and in part due to managers who prefer to have steady businesses rather than spectacular ones. Corzine was not among them, and he couldn’t be. He was hired to take over a midsize trading firm with a specialty in derivatives that had nearly imploded in late 2008. He was brought in to make the firm a powerhouse by taking on the trades that the investment banks most wounded in the financial crisis were cutting back on. In that sense, he likely did what he was hired to do: make big bets. Unfortunately, he did what he wasn’t hired to: make bad bets.

L'affaire Corzine is being treated as more proof of a Wall Street out of control, yet, like what happened with the UBS trader who recently lost billions, the real issue is that the entire incentive structure of trading has shifted dramatically over the past two years, and it is leading to plummeting profitability. Goldman, the firm Corzine once headed and which the Occupy protesters and the Matt Taibbis of the world love to revile, became obscenely profitable in the late 1990s and 2000s largely on the basis of trading profits. The same was true for Lehman et al., and it was the inability of Merrill Lynch, Bear Stearns, and others to keep up that led to their outsize derivative risks and concomitant collapse. What made Goldman so unusual wasn’t risk control per se—though its execs would surely dispute that—but that its traders had a knack for taking the right risks and avoiding the blow-ups.

But in the past two years, as it has become a poster child for Wall Street corruption and a veritable piñata as a symbol of excess, Goldman has become increasingly less profitable. And so have all the others on the Street, from Morgan Stanley and Citi, to lesser-known players. In its recent quarter, Goldman showed massive declines in its trading revenues of both bonds and equities, 20 to 30 percent. The same dismal results were seen across the industry.

The reasons are simple: interest rates around the world are low and trading in a narrow range, except for extreme outliers like Greek debt. Equities are so volatile that even professional traders get whipsawed, and the actual revenues from getting paid to transact trades have been shrinking as machines manage more of those trades for fractions of pennies. There is only one way these companies could make anywhere near what they were making a few years ago: take huge gambles, do what Corzine did at MF Global, and hope they go well. Bet on black and hold your breath.

Most firms won’t do that. The risk of implosion is greater than the rewards of being right. Even if MF Global’s exposure to European debt had gone well, it might have made billions and doubled or tripled its profits, but the risk of being wrong isn’t seeing those profits cut in half: it is seeing the business obliterated. In the new normal of Wall Street, the reality is a bizarre combination of individuals who expect the rewards that came with the risks of the mid-2000s with an industry that cannot hope to replicate those rewards except with a level of risk that is akin to climbing Half Dome in the dark during a snowstorm without a rope.

The diminution of Wall Street is well underway. The market capitalization of the leading firms has shrunk, and the percentage of profits accruing to financial institutions has receded. Yes, these are still hugely profitable businesses, but more in sync with the profitability of Silicon Valley and industrial companies. In the 1960s and 1970s, Wall Street was a niche industry, with its stars and fortunes, but not commanding 30 percent of all profits of all companies in the United States. It was an industry of grit and greed, but one more in balance relative to the rest of society. It is now quickly receding to that once again.

You wouldn’t know that given the animus of protesters, or given the mindset of many of those who staff and lead these companies. But MF Global is proof that the choice is increasingly between foolish, deadly risk and a steady, unspectacular, and less lucrative future. Corzine and MF Global are the klaxon. The battle between the protests and Wall Street isn’t heating up. Wall Street has lost. Whether that benefits the 99 percent remains very much in doubt.