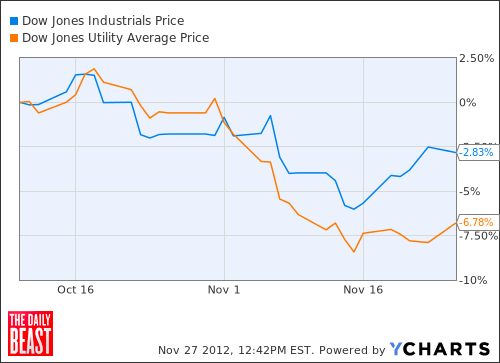

Investors and analysts are looking for signs that the advent of the fiscal cliff is affecting the economy and the markets. The chart above shows one obvious effect.

The stocks of utility companies occupy a particular niche in the investing world. People don’t buy the shares of Con Edison and Exelon in the hope that they will double or become the next Apple. They buy them because they generate steady profits and pay steady dividends. They are expected to produce income rather than capital gains. For the last several years, that income has been lightly taxed. The Bush tax cuts reduced the tax rates on dividends to a maximum of 15 percent.

Come Jan 1, however, if no deal is made, tax rates on dividends will revert to their pre-Bush levels. They will be taxed as ordinary income. So a wealthy person in the 33 percent income-tax bracket would have to pay a 33 percent tax on stock dividends. That would sharply reduce the after-tax value of the dividends. And, because these stocks are valued in part on the basis of the after-tax dividends they throw off, the fiscal cliff would appear to be bad news for utility stocks.

The chart above shows that since the middle of October, when the smart money coalesced around President Obama’s reelection and started to fret over the survival of the Bush tax cuts, utility stocks have been on the decline. The Dow Jones Utility Average has dropped almost seven percent since Oct. 10, while the Dow as a whole has declined a bit under 3 percent. That’s not quite falling off a cliff. But it’s still a significant gap.