opinion

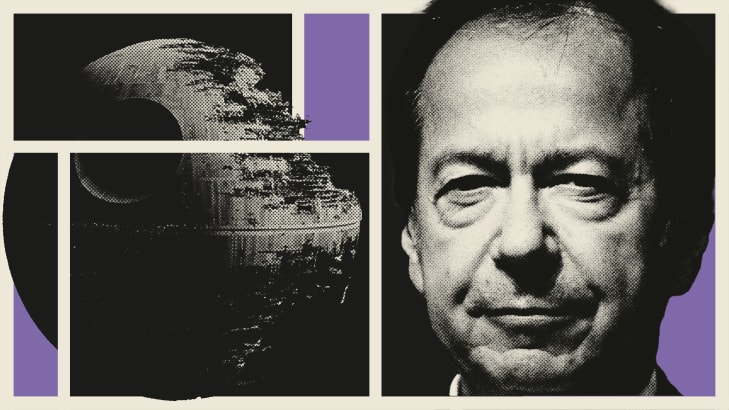

NYU Should Rip Trump Backer’s Name Off Its New ‘Death Star’

CODE BREAKER

John Paulson donated $100 million for the building. Most students have no idea about his MAGA ties.

What to Know About the School Barron Trump’s Graduating From

‘A GREAT STUDENT’

All of RFK Jr.’s Possible Brain Worms, Ranked

BREAKOUT STAR

‘Mommie Dearest’s Rocky Road to Becoming a Cult Classic

IT TAKES A DIVA

CHEAT SHEET

TOP 10 RIGHT NOW

OR

Newsletter

Everything we can’t stop loving, hating, and thinking about this week in pop culture.

By subscribing I have read and agree to the Terms of Use and Privacy Policy.