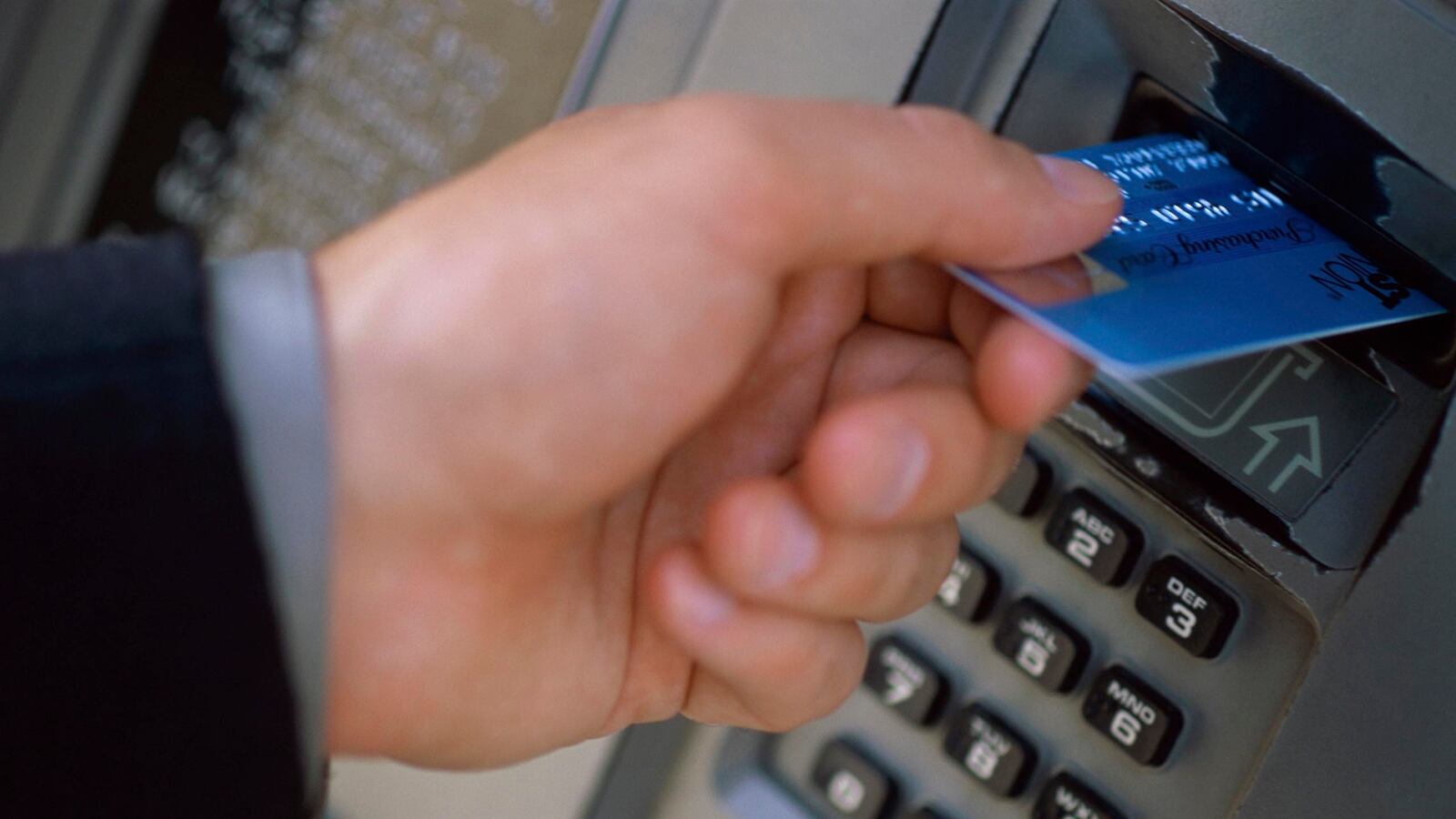

ATMs have served us well for more than 40 years now, but it's time for a reboot.

We trust these machines to dispense cash and accept deposits. But it turns out they can do much more, and more quickly and efficiently, when remote human tellers are involved in the transaction.

The new interactive teller technology from NCR accomplishes that.

Because these machines let people talk to a remote teller on a video monitor, customers can do things that wouldn't be possible otherwise. For example, if you lose or forget your ATM card, you can prove your identity by showing the teller a driver's license.

This is not a simple video chat. The teller on the screen is controlling that machine and all its functions.

"We're creating a personalized interaction that's very secure, but also with very high functionality," said NCR Vice President Brian Bailey.

Because a human is at the helm, an interactive teller can cash a check to the penny and disburse bills in any denomination you request. Want singles or fives rather than 20s? That's not a problem at this ATM.

Another benefit: faster service. Because the remote teller doesn't have to count cash or physically enter the amount of each check—the machine does it—transactions are conducted more quickly than they would be inside the branch.

NCR has about 350 interactive tellers in service, and Bailey predicts that the technology will be in widespread use within the next 12 months. "We're finding that consumers' trust ... is really off the charts," he told me.

The executives at Coastal Federal Credit Union in Raleigh, North Carolina, certainly believe in the technology. Its 15 branches no longer have tellers on site—they've all been replaced with interactive tellers.

"They're more convenient, faster, and safer—robberies basically go away with this—and they allow us to provide better service," said Willard Ross, chief retail officer at Coastal Federal. "Customer response has been fantastic."

By switching to this system, the credit union was able to extend its hours from 7 a.m. to 7 p.m. seven days a week.

Steve Ferrani, who uses an interactive teller at least once a week for his business deposits, appreciates the longer hours.

He also likes having those deposits posted to his account sooner. It typically takes a day or two for processing a deposit made at a traditional ATM, but because Coastal Federal's interactive teller can verify the deposit in real time, it's credited that day.

By the way, the machines work like any other ATM unless the customer pushes a button to request a human teller. Analysts believe it's critical that customers decide when they want to do a totally self-service transaction and when they want some help.

"If you make the teller available on demand, only when requested by the consumer, then those types of transactions are more likely to be done at the ATM," said Bob Beara, a senior analyst with the research firm Celent. "And that's good for both banks and their customers."

Bank of America believes remote tellers will help it build a deeper relationship with customers. In April, it began installing the first ATMs with what it calls Teller Assist in Boston and Atlanta. The bank plans to fast-track deployment through 2014.

"This is the future of banking," said Shelley Waite, Bank of America's senior vice president for ATMs. She calls the new technology "groundbreaking" because it lets machines do 80 percent to 90 percent of what a teller inside the branch can.

Right now, customers using a machine with Teller Assist can talk to that virtual teller in English or Spanish. More languages could be added in the future.

"The feedback has been tremendous," she said. "Some customers are surprised there's somebody right there who asked them about the weather and helped them with the transaction."

If you had the choice, would you rather use your debit card or your smartphone to access your account at an ATM? Given the insatiable appetite for apps, some bankers believe they must embrace the mobile option.

Diebold, which makes more than half the ATMs in the U.S., just announced the first machines with Mobile Cash Access.

"I think it will be adopted fairly quickly," said Jim Block, director of advanced technology at Diebold. "It gives people a combination of convenience, security, and control, which makes it a very lucrative mechanism to integrate with banking."

Wintrust, a financial holding company that owns 15 community banks in greater Chicago and Milwaukee, will be the first to roll out Diebold's mobile-enabled machines. The company is testing a few machines now, and if all goes as planned, the bank's entire fleet of 180 ATMs will offer this service before the end of the year.

With the Mobile Cash Access app, customers can preload transactions at their convenience. When they get to the ATM, they just push a button and a QR code comes up on the screen. The phone reads the code and tells the machine what you want to do. If you requested cash, the money is dispensed and an electronic receipt is sent.

Those prestaged transactions take only about 10 seconds, according to Thomas Ormseth, executive vice president of retail strategies at Wintrust.

Because no card is involved, Mobile Cash Access eliminates the risk of skimming, in which an identity thief steals your account number as you insert the card into the machine.

The phone is secure because your account information is stored in the cloud, not on the device. You must enter a PIN to use the app. And because you get a text or email after each transaction, you'd know right away if someone gained access to your account.

The bank expects big things from this technology.

"We'll be very happy if we get 20 percent market penetration next year and we can prove that we've gotten some new customers because of it," Ormseth said. "Given the feedback we're getting, I do think this is realistic."

By CNBC contributor Herb Weisbaum