President Donald Trump’s threat to “obliterate” Iran’s energy infrastructure if they don’t bow to his demands has created market madness and the potential for an unprecedented crisis.

Trump appears to have grown increasingly irate with Tehran’s refusal to allow tankers to ferry Gulf energy around the globe by effectively choking the narrow shipping lane, the Strait of Hormuz. On Saturday evening, he delivered a stark ultimatum: open up in 48 hours, or face bedlam.

Iran has refused to obey, instead warning of revenge attacks if Trump went through with his pointed threat. As the clock ticks towards Monday evening’s deadline, the potential for disaster has triggered all-out financial panic.

In fact, the global economy faces a “major, major threat,” according to the head of the International Energy Agency.

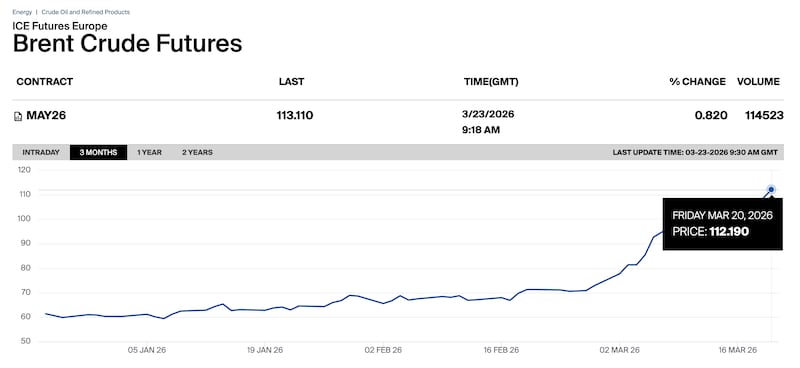

Speaking on Monday, as Israel continued to attack Iran and the benchmark price of oil ticked up 1.5 percent to $114, Fatih Birol warned just how far-reaching the consequences of the conflict could become in less than 24 hours. “No country will be immune to the effects of this crisis if it continues to go in this direction,” he said at Australia’s National Press Club in Canberra.

The situation is so “severe,” he argued, that it is already worse than the two previous oil crises combined.

The oil crises of 1973 and 1979 were two of the most economically damaging energy shocks of the 20th century. The first was triggered by an Arab oil embargo against Western nations that had supported Israel in the Yom Kippur War, causing prices to quadruple almost overnight and plunging much of the Western world into recession. The second followed the Iranian Revolution and the fall of the Shah, which severely disrupted Iranian oil exports and sent prices spiralling again—a crisis deepened further by the outbreak of the Iran-Iraq War in 1980.

Birol said the resulting market turmoil meant a reduction of 10 million barrels per day leaving the Gulf, causing “major economic problems around the world, the recessions. And today, only as of today, we lost 11 million barrels per day.”

After Russia’s invasion of Ukraine in 2022, the gas markets, especially in Europe, were debilitated, Birol added. They “lost about 75 billion cubic meters, 75BCM. And as of now, as a result of this crisis, we lost about 140BCM, almost twice (as much).”

Echoing Trump’s requests, he surmised, “The single most important solution to this problem is opening up the Hormuz Strait as things stand now.” For now, his agency is deliberating on the release of more stockpiled oil to meet demand and quell market turmoil.

The situation took a turn for the worse following Trump’s threat over the weekend. “The United States of America will hit and obliterate their various POWER PLANTS, STARTING WITH THE BIGGEST ONE FIRST!” he ranted in a Truth Social post. Global benchmark Brent rose above $114 a barrel, up for a fifth day in a row, according to The Financial Times, while West Texas Intermediate was near $100.

The ongoing blockage of the Strait of Hormuz means that Brent is expected to average $85 a barrel in 2026, up from an earlier forecast of $77, according to analysts.

Also amid the turmoil, European stocks entered correction territory and U.S. futures pointed to losses of around 1 percent on Wall Street. Gold fell more than 8 percent, according to Bloomberg, while the FT said silver tumbled by 10 percent.

“Now with this 48-hour deadline, Trump has posted himself into a corner,” Rory Johnston, oil market researcher and founder of Commodity Context Corp, told Bloomberg. “It is highly unlikely that Tehran will agree to Trump’s terms on such an accelerated timeline under the threat of attack. And Iran is clearly able and willing to match any escalation.”

The White House has been approached for comment. Explaining Trump fanning the flames and upsetting global markets, his Treasury Secretary Scott Bessent on Sunday said, “sometimes you have to escalate to de-escalate.”